When asked what he viewed as mankind's greatest invention, Albert Einstein reputedly replied,

“Compound interest is the Eighth Wonder of the World. He who understands it, earns it; he who doesn't,

pays it.”

Mathematically, performance compounds and fees decompound, i.e., exponentially increasing

and damaging the value of your portfolio, respectively. We’ll see in a moment that the interplay

between performance and fees is computationally complex and not always intuitive; the finance

industry understands it and retail investors mostly don’t.

As a consequence, retail savers become a sitting duck, vulnerable to one of the largest unspoken

wealth transfers in the UK.

Setting the maths aside for a moment, one can think of it like this: Drive your car with low quality

motor oil and it’s not poor machinery that will destroy your engine, it’s the friction. In the same

way, unfair fees will destroy an otherwise resilient repeat-purchase investment portfolio which

invests in sound assets generating high, compounding returns on invested capital.

In terms of performance, Part 1 of Eriswell’s “Behind the Curtains” series examined the poor

returns achieved by the retail investment industry and for example why, according to the CFA’s

(Chartered Institute of Financial Analysts) calculations, active funds underperform by over 1.5%

per annum. This underperformance would cost you 25% of your savings every 20 years.

What is the price of such poor outcomes? Wealth and investment management fees remain

stubbornly high and largely immune to poor performance.

We explore:

Becoming a minority holder in your life!

Total fees in the UK for an advised retail portfolio typically range between 2.25% and 3.5% per

annum, with an average of 2.83%*.

While optically small, paying 2.83% annual fees will turn you into a minority holder in your own

life after 25 years!

To see this in practice, you might think of the fabulous buildings which dot the City of London.

Look deeper and you will notice that UK asset managers earn an average operating margin of

38%, compared to just 16% for the FTSE All Share Index.

Let’s take a look at the numbers:

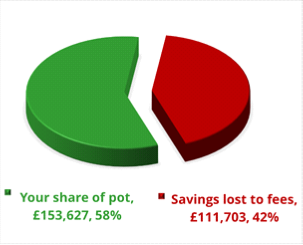

Invest £100,000 at a 5% return annually and it will grow to £265,330 in 20-years, representing a

cumulative gain of 165%.

Now deduct typical total UK investment fees of 2.83% per annum and that same £100,000 will

increase to only £153,627, representing a cumulative gain of just 53%.

Your final pot has lost almost half its value! (Chart 1)

Up comes the crossover point after 25 years, the balance point when the finance industry has

reaped the benefit of 50% of your hard-earned savings. On the process goes:

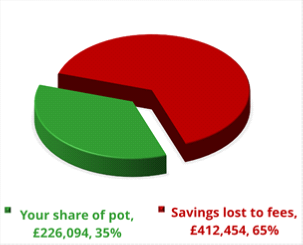

Over an average 38-year UK working life, fees alone will go on to reduce your final saving’s

and pension pots by a staggering two-thirds (Chart 2). Don’t worry if this seems

counterintuitive, that kind of maths astounded even Einstein!

Add poor performance into the equation and you end up in a far worse position than you could

have been under a simpler, lower fee, better performing, and more passive portfolio.

This doesn’t seem like a fair deal for savers. And having spent a lifetime in hedge funds – we

agree!

Chart 1: Your Savings after 20 years Chart 2: Your Savings after 38 years

* Industry standard UK combined fees for a £100,000 investment are 2.83% per annum.

Decomposition as follows: 0.95% per annum Wealth Management/IFA advice; 1.25% p.a. active fund

management fees (OCF + hidden transaction charges); and 0.63% per annum additional fees,

including inter alia entry/exit fees, bid/offer spreads, and administrative charges. Sources: FCA,

ESMA, Market estimates.

Fees, fees, and more fees

UK financial advisors and wealth managers typically charge 0.5–1.5% per annum of total asset

under management via what are known as “ad velorum” fees. Additional costs are incurred to

wrap investments into tax-efficient structures such as ISAs, SIPPs, Personal Pensions,

Onshore/Offshore Bond, etc. Then there are transaction fees, initial fees, redemption fees,

foreign exchange fees, security borrowing costs, brokerage fees, nominee fees, advisory

commission fees, and sometimes performance fees.

Some of these are included in the fund’s regulatorily mandated OCF (ongoing charge figure) but

many aren’t.

Finally, there are the ‘hidden fees’ charged in jurisdictions that still allow inducement

commissions to be paid by investment funds, life insurance policies, and pension products to the

wealth manager/financial advisor.

A European Commission study summed-up the problem like this:

“Products are recommended to clients not based on their merits, but instead based on those which

generate the highest commission for the adviser.”

Why do people accept high fees for subpar performance?

The answer has to do with human’s inability to react to sinister threats that arise gradually as

opposed to suddenly. The boiling frog metaphor is sometimes used as a warning: If a frog is

suddenly put into very warm water, it will jump out; but if it is put into cool water which is then

gradually warmed, the frog will not perceive the danger and will be slowly cooked to death.

It turns out frogs are not that stupid; they recognise the problem and leap out of the water in

time.

In fact, frogs perform better than humans! Harvard psychologist Daniel Gilbert found that

while human brains are well adapted to respond to immediate threats such as a fire, a sinking

ship, or terrorist attack, we display an inbuilt unwillingness or inability to react to sinister threats

like global warming that arise gradually over time.

Or the threat that our retirement and future lives drown under the combined weight of poor

performance and high fees.

One’s stress levels, however, slowly rise

Media outlets constantly run stories about how people are destined to live in penury by not

saving enough for their retirement. Rarely is the blame laid at the feet of the finance industry but

that, as they say, is another story.

Being forced to confront one’s financial future is a stress everybody will feel at some point.

Your brain responds by releasing cortisol to prepare a fight or flight response. Your heart rate and

blood pressure increase, glycogen is released into your bloodstream to provide energy and your

immune system prepares itself for injury.

If the threat passes, cortisol levels will swiftly drop, and your body will return to normal.

But if these financial worries persist, your cortisol levels become unstable, and you may

experience physical symptoms including high blood pressure, an irregular heart rate, anxiety, and

a difficulty to concentrate.

A prolonged state of fear ultimately reduces our capacity to make sound judgments and rational

decisions just when we need it most!

The moral of the story is clear: whether you’re saving for a house, your kids’ education, early

retirement, a new business, anything you like.

Act now! Put in a plan in place, save enough, and make sure your money works hard for you not

everybody else.

How do sophisticated investors cope?

Whether they be hedge funds, large endowments, or sovereign funds, the most world’s most

sophisticated investors are well aware of the dangers posed by high fees. To the point of rating

fees alongside reputation, past performance, and 5-star ratings when choosing a manager.

Sure, they will pay high fees to a top hedge fund, but they will demand top performance in return.

In addition, professional investors negotiate hard and rarely pay anything like what retail

investors pay, even for access to the same funds.

Why are regulators not doing something?

They are, but change is happening at a snail’s pace. The FCA notes that investment returns are

“materially impacted by weak price competition.” European regulators, meanwhile, make the

following comments:

•

“We have found that on average, retail investors in both active and passive funds underperformed

their benchmarks net of costs.”

•

“Complex charging structures mean consumers may struggle to assess the value for money

offered, and can also end up overpaying for services from advisers and platforms. This is

especially true where opaque charging makes it difficult to assess what services are being

provided within the product.”

Elsewhere, regulatory studies have found:

a.

No clear relationship between higher fees and higher performance.

b.

An industry-wide reluctance to undercut each other, economies of scale captured by

advisors and fund managers not the retail investor.

c.

Evidence of widespread passive indexing (when an active fund charges active fees but then

simply tracks the index).

d.

High salaries and poor cost control ultimately borne by retail investors, not their advisors

and fund managers.

Why can’t regulators put a stop to this?

Part of the problem is that, unlike the frog, retail investors struggle to grasp their predicament.

And if retail investors don’t grasp their problem, they are unlikely to act, even if the regulators

mandate that a solution is made available to them.

On this point, a 2013 OECD study found that 61% of UK investors struggled to understand

compound interest, with only 39% of respondents able to correctly answer basic questions. Other

studies found that savers make the worst investment decisions when the best choice was given

as a percentage, and that retail investors struggled to identify the best choices when

performance and fees were not computed over the expected lifetime of their investments.

None of this is lost on financial institutions: They have grown adept at turning to their

advantage gaps in people’s understanding of finance and mathematics.

Conclusion

Investing is in many ways like rearing a delicate flower; space must be given for investment flair

and talent to bloom in the context of a disciplined and carefully controlled environment.

Toxic fee levels are a sure-fire way of causing your plants to wilt.

How can we solve this complex problem? Part 3 of this series will outline the risk

management, asset allocation, and fund governance controls deployed by some of the world’s

largest and most sophisticated investors.

Do you truly know your total advisory and portfolio management fees? If not, think about why.

Andrea Badelt, Partner

How Fees destroy your Savings in Time

Behind the Curtains of the Assert Management Industry #2

BY ANDREA BADELT, PARTNER

Eriswell Market Insights

| 21 July 2021

+44 (0) 1932 240 121

info@eriswell.com

© 2024 Eriswell Capital Management LLP