The ‘house edge’ is 0.5–2% in Blackjack, 1.4–5% in Craps, and 5.3% in American Roulette

(two zeros).

A red or black bet on the roulette table gives you a 47.37% chance of winning. But hey,

you’re in Las Vegas to have fun; you’ve saved up for that dream trip and you know the

money in your wallet won’t be there as you head back to the airport.

Buying an active fund is a bit like paying someone to play Roulette for you, only these are

your life savings and not fun money. The stakes are high: If the player wins – you could

make a lot of money, if they don’t it will affect your future life outcomes.

Like any gambler, promoted funds are those flush from a recent win. Can they really beat

the Stock Market Casino, or were they just lucky?

That is the question.

It turns out that your odds of success in choosing an active fund are far far worse than

you’d get in Las Vegas. To demonstrate this, I’ll use the latest data from S&P Dow Jones

Indices.

At the end of June 2019, S&P identified the top quartile of US active equity funds,

then followed their progress over the next two years.

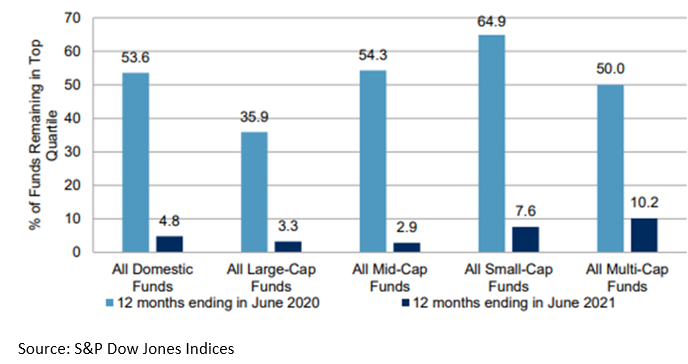

At the end of June 2020, some 53.6% of these top quartile funds remained in the top

quartile, more than we would expect by random luck (Figure 1). This opened two

possibilities: (a) these managers were truly good, or (b) the stock market winners in the

run-up to the Covid pandemic kept winning throughout the lockdown.

Roll forward another 12-months and by the end of June 2021, we can see that the

‘superstar’ funds had fallen back to earth with a thump, with a mere 4.8% remaining in the

top quartile.

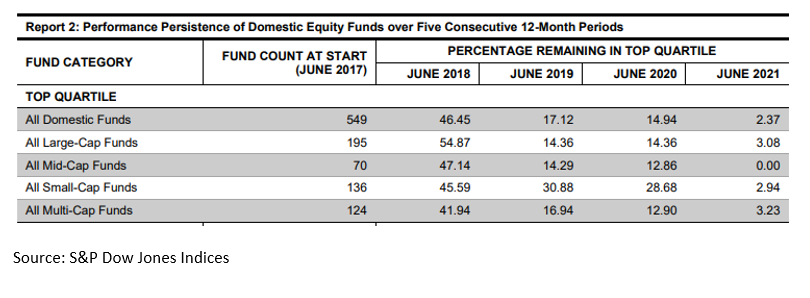

Starting with top-quartile funds as at the end of June 2017, just 2.3% remained in the top

quartile four years later in June 2021 (Figure 2). The best outcome was 3.2% of Multi-Cap

Funds, whereas not a single Mid-Cap Fund survived the cut.

Fixed income and European asset managers fared little or no better.

Had you invested in a top quartile active stock fund in June 2017, you would have had only

a 3.2% chance of remaining in the top quartile four years later.

On a 10-year horizon, this translates to a mere 8% chance of just matching the S&P500

index.

They are shut down or merged. Fourth-quartile funds are typically folded after a few years,

freeing the manager in question to spin the wheel again with a new fund.

“The value of investments can go down as well as up and you may get back less than you

invest.” It’s everywhere.

The finance industry, however, knows that few heed such warnings, just as few heed the

UK’s online gambling warning: “When the fun stops, Stop!”

And be aware that fund marketing departments are skilled in playing the behavioural

biases that delude us into chasing trends, and our feelings of regret at not being in a

winning fund.

So, now you know.

As to what to do about it, that’s another story – many stories in fact! We’ll explain ours this

side of Christmas.

As ever, any and all comments welcome either below or at info@eriswell.com

Mark Page, Managing Partner

Figure 1: Top Quartile Funds in June 2019 performed well for 12-months then fell back to

earth

Figure 2: