I find it implausible that central banks who approached 2022 at what in monetary terms was

the speed of heat, would not have known the basic things they needed to do, to avoid a violent

collision with inflation.

They too had seen the forecasts of Eriswell’s or similar zero-r* models, right?

Moreover, central banks knew these zero-r* models were on a roll, and that their latest

forecasts were turning from bleak to dire. So, what caused people, who couldn’t possibly

escape knowing where the risks of inflation come from, reach a point where they became so

utterly complacent as to destroy the lives of many, while being too blasé to lift a finger?

One explanation is what psychologists term continuation bias: “We’ve monetised like crazy and

haven’t blown up yet, so let’s press on.” Another explanation is what accident investigators

describe as human’s inability to recognise that everything is going almost unimaginably wrong.

Target fixation and groupthink may also play a role. Or perhaps, so many have Cried Wolf on

inflation since 2008 that central banks stopped listening, choosing to rely on their obsolete

inflation models instead.

Or maybe this model mania is part of the problem: where protagonists from central banks

to monetary hawks, to the zero-r* outriders like Eriswell, all fiercely defend the supremacy of

their belief and mathematical systems.

Perhaps what is missing is basic situational awareness of what is going on out there that

could kill us, and an understanding of how can we stay away from that? The starting point

is to reject the old bromide that, on 24 February, we woke up to a different world; Ukraine

significantly exacerbated inflation but didn’t cause the problem and to argue otherwise is

ludicrous.

And if central banks and governments either can’t or won’t get this right, then you as

investors most certainly must.

In the meantime, why would we have any confidence in central banks to now get us out of this

mess? Why do we even listen to them!

We’ll be navigating alone a while now and must be very careful and very engaged with the data.

Simple example of situational awareness

By this we mean maintaining a situational awareness of the evolving backdrop that will

configure what governments and central banks will actually do, no matter what they

have committed to doing. For example, this simple data that tells us that the UK Government

will indeed be distributing handouts this autumn and that the Bank of England will indeed be

monetising more debt, if necessary, EVEN with inflation running hot and sterling heading for

the dustbin.

This is nothing to do with fancy r* stuff, and all to do with the basics of social stability and

harmony.

You’ve all seen charts like Fig 1 which depict the post-pandemic bounce in real UK pay. Which

the Government and BoE cheered as evidence the UK economy was finally delivering decent

real wage growth after several years of negative/near-zero growth.

Lacking basic situational awareness of what is going on out there that could kill them, the Govt

and BoE didn’t spot the imminent danger, and blundered onwards into ‘graveyard spin’.

Spiralling down almost to the ground before realising what was happening. Then came two

comically opposing claims:

•

We are confident in making a soft landing! …and

•

It’s not our fault if we crash !!

Whose fault is it then? Who was piloting the aircraft? It’s the type of problem every pilot is

trained for, the BoE’s inflation instruments aren’t working so it needs to look around to see

what’s going on. And then fly on visual.

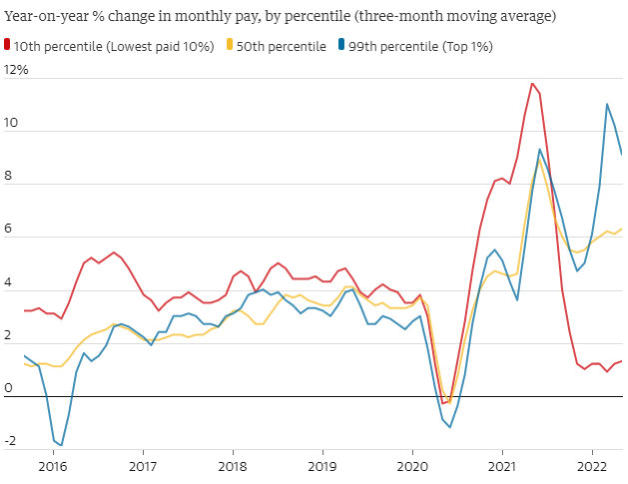

Take the latest implorations of wage restraint to lower-paid workers – look at Fig 2. The bottom

10% of earners have received an almost zero increase in nominal wages, meaning the poorest

families are now experiencing a 10% to 20% contraction in their spending power. There are

technical reasons for this including the minimum wage, but the point stands.

How does this square with c.10% inflation? Because poor families spend much more of their

incomes on heat, food, and shelter than the rest of the population. And that’s before they get

sucked into emergency credit facilities for which high street banks will charge them between

22% and 28% for when they can no longer make ends meet. Loan sharks beckon when these

credit lines are exhausted.

This simply won’t work, it will be morally unacceptable to the majority of the population. And

so, the UK Government and BoE will either bend to the social will or face fairly instant

termination. FX traders have spotted the catch, other asset markets will follow.

Fig 1: Both real total and regular UK pay fell on the year, with a record fall for real regular pay

Source: ONS

Fig 2: Top 1% of earners collecting 9% nominal pay rises while nominal wages have hardly risen

at all for the lowest paid

Through the Eyes of a Hedge Fund Manager, Series #14

| 22 August 2022

Eriswell Market Insights

What is out there that can kill us?

BY MARK PAGE, MANAGING PARTNER

+44 (0) 1932 240 121

info@eriswell.com

© 2026 Eriswell Capital Management LLP