2020 opened with many classical threats to financial markets: war in the Middle East, oil spike, nuclear

conflict, simmering trade tensions, political instability, global energy inequality, and Brexit, etc.

What should we make of them? Despite these risks being generally well analysed, there is a marked

tendency for investors to overplay farfetched financial contagion scenarios that historical precedent

suggests are much less likely than commonly imagined.

On the other hand, financial crises tend to be driven by factors beyond the scope of conventional

process-driven risk management techniques that don’t lend themselves to breathless live reporting

and, most curiously, which are beyond the scope of our collective imaginations.

Just such a factor exists today.

Conventional risk management can actively increase systemic risk

Financial risk management concerns itself with the management of significant but unlikely adverse

events. It is an inexact science where no single technique provides a full solution; value at risk (VAR),

extreme value theory (EVT), and adverse scenario analysis all play a part.

It is well accepted that VAR-based tools are more concerned with the management of short-term

volatility than protecting against extreme events. This has in the absence of something more

imaginative led to an overreliance on adverse scenario analysis with its inbuilt bias towards preventing

a repeat of past crises: 1987 Crash, 1997 Asian Crisis, 1998 Long Term Capital Management, Russian

default, 2000 Tech Bubble, 2008/09 Great Financial Crisis, etc.

It is also well accepted that diversification – a foundation stone of risk management – can be

counterproductive at a macro prudential level. For example, between 2003 and 2007, and again

between 2013 and today, the trend towards increased risk diversification exerted and is exerting a

downward pressure on asset price volatility generally.

Everything looks safe during this low volatility period, but hand in hand comes an increased

risk that difficulties within a particular asset class swiftly spillover to other unrelated assets

and jurisdictions, the so-called contagion channels.

What might trigger such a crisis today?

The answer is probably not a big shock event

To see this, we must first step away from the collective obsession with sudden adverse events. True,

most sudden events tend to be bad news: wars, terrorist attacks, unexpected Federal Reserve move,

imposition of new tariffs, SARS outbreak in China, etc. Like Iran this week, they attract vast media

coverage but tend to affect asset prices by less than one might expect.

By comparison, most things that happen gradually over time are good: prolonged recession-free

period, an extended peace, improving education, medical advances, etc. In economic terms, the most

powerful driver of today’s economies and markets is just such a slow-burn factor – the ‘magic of

productivity’ – i.e. the ability to produce more and more from the same economic inputs.

Human’s irrational dread of catastrophe fuels an irrational fear of sudden losses (Kahneman/Tversky),

which in turn creates a ready market for the prophets of doom. At times of heightened tensions – like

today – these voices appear across the media with warnings of impending disaster, ostensibly based

upon their savvy reading of geopolitical events and market trends. In practice, it is more to do with

their skill in weaving narratives that arouse our sense of horror. Fears which are subsequently

magnified by our innate difficulty in distinguishing between 1-in-a-million chances and a 1-in-a-

hundred ones.

These prophets of doom are invariably wrong, assets remain hooked in the objective reality, and

investors talk about climbing the wall of worry. Pretty much what we are seeing today.

While not the answer to what might cause a financial crisis, these excessive worries have a dangerous

side effect.

A masked factor has developed behind the scenes

Amos Tversky made much of humans’ inherent irrationality in dealing with probabilities and in

particular contingent probabilities. For example, we intuitively think of the risk of two adverse events

occurring simultaneously as very unlikely, even if we know that flipping a coin once doesn’t change the

odds of a second flip. This is a big problem in finance, not for want of maths skills, but because when

probabilities become correlated, as they inevitably are where collective risk diversification has taken

place, then the chance of one adverse event leading to another, however unlikely this may seem if

separately evaluated, increases significantly. The outcome in cases where such contagion channels

exist is much worse than a statistician might judge based upon past data alone.

In other words, a second risk can become obscured behind the perceived unlikelihood of a first

big headline news story such as Iran. And especially – as is the case today – if that second risk is a

slow-burn, non-newsworthy factor that can evade detection from conventional risk systems by actively

supressing volatility. Even more dangerous is when this second risk can also evade extreme value

analysis through lack of historical precedent.

Most potent of all are those factors with the potential to first magnify asset prices to the point of

actively fomenting asset bubbles, then decimating them when growth and corporate earnings stutter.

Enter the entrenched productivity stall: and the persistent misunderstandings as to its ultimate

destiny in liquidity trap conditions.

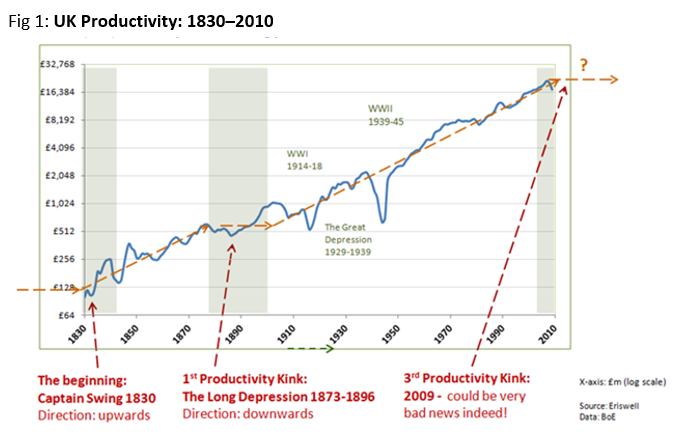

The slow burn obscured factor: wonder and danger of productivity

The Wonder: while possessing no momentum in a literal sense, productivity’s steady G-7 post-1880

annual growth rate of 2–2.5% certainly suggests the existence of an underlying constant, the

‘productivity metronome’.

Recessions temporarily interrupt this trend, although in normal circumstances the 2–2.5% productivity

trend continues in background. Technology, science, and medical progress continue to offer new

efficiency savings through improved technology, better public health, and increased knowledge. Which

sets the scene for the V-shaped recoveries that propel the post-recession economy, not only back to its

original level, but upwards to regain its long-term productivity trend (Fig 1).

When productivity stalls: economic productivity (output/hr) is different to technology progress. The

glue that normally binds the two is, when technological/scientific progress can create new more

productive jobs to hoover up the workers displaced by efficiency savings elsewhere. However, every

60-100 years this glue ‘mysteriously’ fails, and the so-displaced workers are forced into lower-paid,

less-skilled work. At this point the economy enters a productivity stall which tends to persist for 20

years or more.

During such periods, fiscal and monetary policy both play a role, the latter by stimulating households’

and corporates’ innate preference to inter-temporally forward-shift consumption, investment, and

profit. The hope is that economic productivity’ will soon restart. This was the story of the Europe/US in

1873-1896, Japan 1986-2018, and Europe/US 2008 -?.

There is currently little visibility as to where all these well-paid more productive jobs will come

from. Which is a BIG PROBLEM because the credit-based intertemporal forward-shift in consumption

is finite.

That said, the current thinking within Western central banks (despite the ECB’s repeated denials) is that

improved developed market’s private sector balance sheets no longer pose a risk and that central

banks can safely manage government debt much higher if necessary. In the same vein, these same

central banks believe that China possesses the necessary fiscal space to smooth any blowouts in its

ballooning private sector debt (Fig 2).

Do you believe that central banks can safely walk the debt monetisation tightrope?

The ballooning debt tightrope

Neither do the debt experts introducing the excellent new World Bank book “Global Waves of Debt”

(well worth a quick read):

“After

a

decade

of

slow

growth

and

low

interest

rates,

the

world

is

awash

in

debt—issued

by

households,

corporations,

and

especially

governments.

It

is

tempting

to

believe

that

with

interest

rates

as

low

as

they

are

today, including in emerging markets, much higher debt levels are sustainable indefinitely.

This

book’s

impressive

review

of

history

and

theory

cautions

against

complacency

and

argues

for

proactive

policies

to

buttress

macroeconomic

and

financial

stability.

All

analysts

of

the

global

economy’s

past

trajectory and future prospects will want to read this book.

Hopefully, policymakers in authority, whether madmen or not, will do so as well—before the next crisis hits.”

Maurice Obstfeld

Berkeley University

One is remined of Jean de La Fontaine’s, “The frog that wished to be as big as the ox”:

“This world of ours is full of foolish creatures too;

Commoners want to build chateaux;

Each princeling wants his royal retinue;

Each count his squires.

And so, it goes.”

The frog never realised it was about to explode! La Fontaine’s analysis applies equally well to

today’s credit fuelled economies (private and government credit).

Conclusion

Western central banks’ ‘worst case’ scenario is spiralling inflation, unexpected and severe rate hikes,

and deep recession. They don’t see that outcome as particularly likely and neither do we. The trouble

is that the difference between their ‘base case’ and ‘worst case’ scenarios is largely irrelevant today.

For the base case is simply managing government debt up to a level where there is no longer a

credible way out. Our in-house Zero Lower Bound models foresee no credible outcomes where a

restart in productivity growth is accompanied by a continuation of near-zero natural real interest rates.

Can you?

Finally, the ‘best case’ future growth scenario revolves around ample new well-paid jobs within

thrusting new frontier industries.

This seems farfetched at best.

Andrea Badelt

The big danger is still the productivity stall

BY ANDREA BADELT, PARTNER

Economies and Capital Markets Series #1

| 10 January 2020

Eriswell Market Insights

+44 (0) 1932 240 121

info@eriswell.com

© 2026 Eriswell Capital Management LLP